Due to the Russian aggression, which began in 2014, Ukraine has suffered significant losses, in particular the occupation of about 18% of the territory and the loss of more than 15 million people. Pharmacy retail has also suffered losses: about 5 thousand pharmacies have closed since 2014. Information about this is provided by Proxima Research based on data from the syndicated database “Axioma”.

Situation with pharmacies in the regions of Ukraine

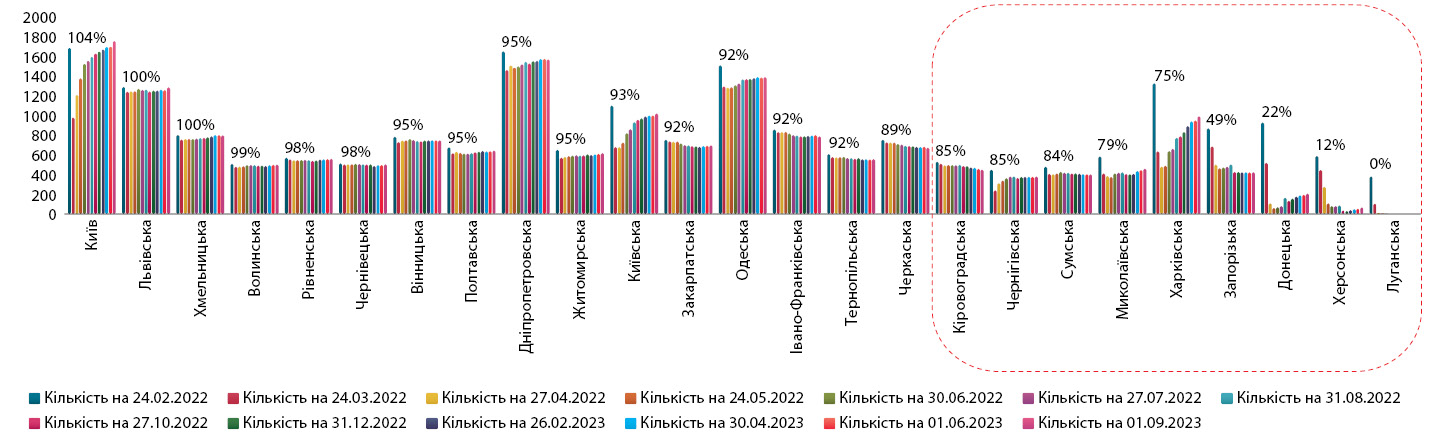

As a result of Russian aggression, the number of pharmacies in Ukraine has decreased in all regions, but the eastern, southern and northern regions have suffered the most. In the territories liberated from occupation, the number of pharmacies is gradually recovering, but in the regions where hostilities continue or a significant part is under temporary occupation, the situation remains difficult.

As of September 1, 2023, only three regions have restored the number of pharmacies to pre-war levels. In most oblasts, the number of pharmacies is more than 90% of the pre-war level. The most problematic regions are predominantly eastern and southern regions, in particular Kirovograd, Chernihiv, Sumy, Mykolaiv, Kharkiv, Zaporizhzhya, Donetsk, Kherson and Luhansk oblasts. In these regions, hostilities continue and a significant part is under temporary occupation, which makes it difficult to open pharmacies. However, in the territories liberated from occupation the process of restoring the number of pharmacies continues.

In the first months of the full-scale war, the number of pharmacies in Kharkiv almost tripled. In May 2022, there were only 227 pharmacies in the city, while before the war there were 772. However, since June the recovery began, and as of September 1, 2023 the number of pharmacies in Kharkiv increased to 614, or 80% of the pre-war level. The sales of medicines in Kharkiv are also growing. In monetary terms, they are 81% of the pre-war level.

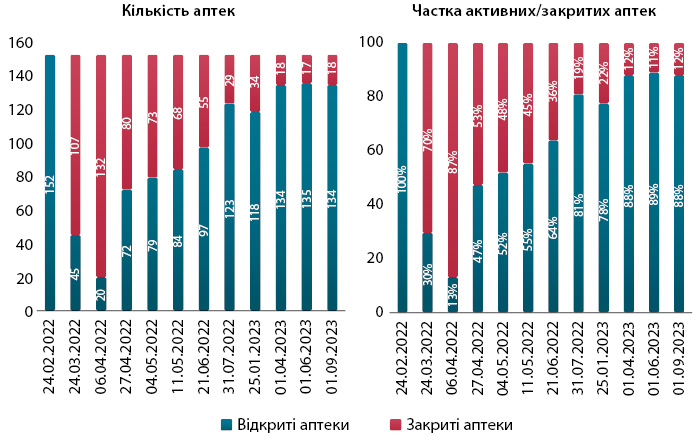

Since the occupation, the number of pharmacies in Kherson has decreased by more than 10 times. After de-occupation, the situation started to improve, and as of September 1, 2023, the number of pharmacies in Kherson is about 30% of the pre-war level. Drug sales in Kherson are also growing, but so far they are only about 30% of the pre-war level.

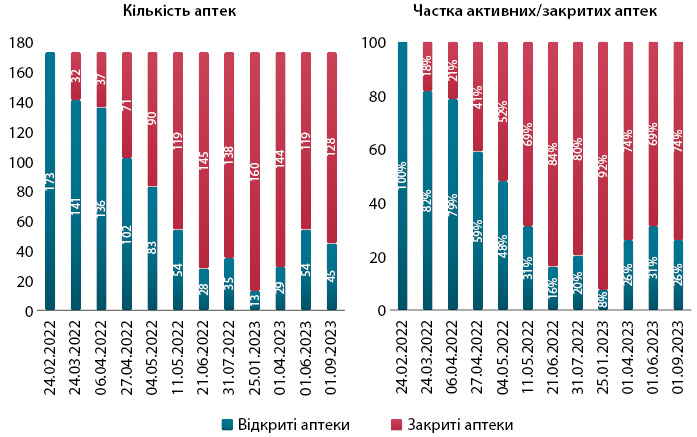

In Chernihiv, the number of pharmacies decreased to 20 in April 2022, 86% below pre-war levels. However, after the city was liberated from Russian forces, the number of pharmacies began to grow rapidly, and as of September 1, 2023, there are 134 pharmacies in Chernihiv, or 88% of prewar levels. Drug sales in Chernihiv are also recovering and are now at 98% of pre-war levels.

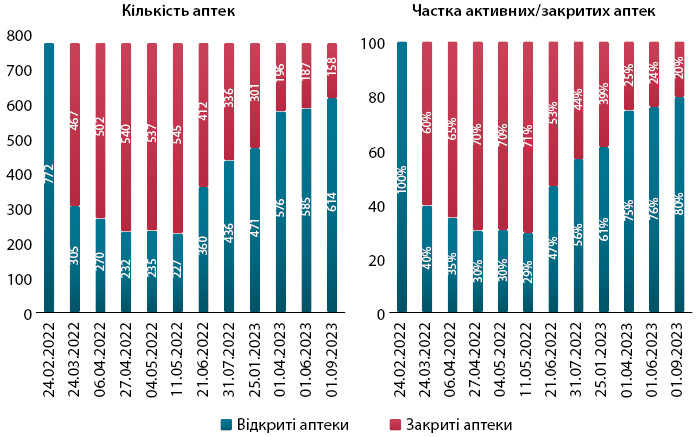

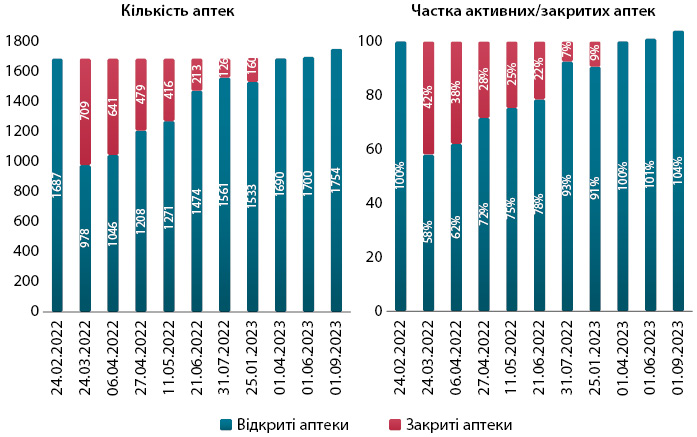

In Kiev, the number of pharmacies decreased to 978 in March 2022, when the city was under threat of occupation. However, after the expulsion of Russian troops, the number of pharmacies began to increase, and as of September 1, 2023, there are 1,754 pharmacies in Kiev, more than in the pre-war period. Drug sales in Kyiv are also growing and have already exceeded pre-war figures.

Pharmacy market leaders

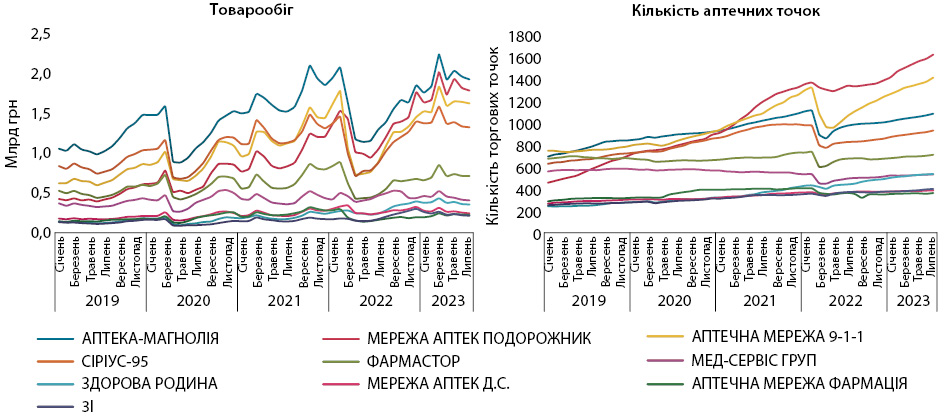

The impact of the war on the pharmacy market varied from region to region. The chains in the west of the country suffered less losses than in the east and south. Therefore, it is still difficult to speak about the achievements or failures of individual players in the market.

In general, a similar trend is observed for the top 10 pharmacy chains in Ukraine. At the beginning of the war, there was a significant drop in turnover and the number of pharmacies. However, since July 2022, recovery started and most chains have reached their pre-war turnover figures.

In January-July 2023, the ranking of pharmacy chains by turnover in money terms was headed by: APTEKA-MAGNOLIA, PODORozhnik Pharmacy Chain, 9-1-1 Pharmacy Chain, SIRIUS-95 and PHARMASTOR, which accumulate 57% of the total turnover in money terms and the share of the leader is 14.8% (table).

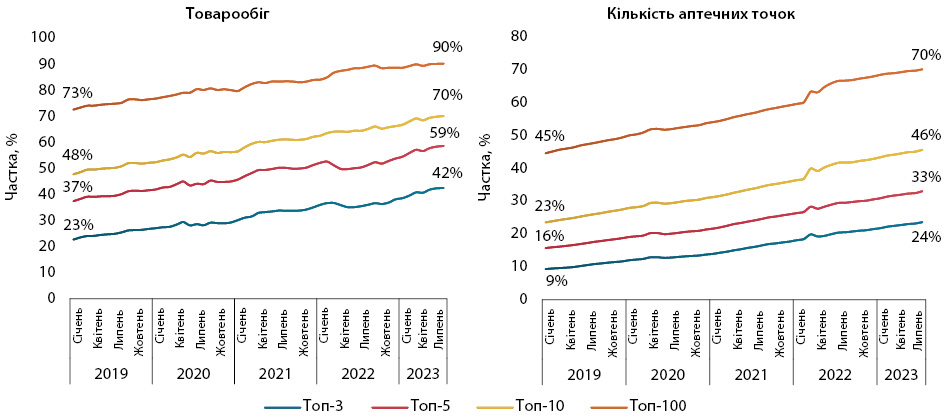

Consolidation of the pharmacy market continues

Even in the conditions of war, consolidation of the pharmacy market continues. At the beginning of the invasion, the process slowed down, but then started gaining momentum again. As of July 2023, the top 10 pharmacy chains have 70% of the market by turnover and own 46% of pharmacies. For the top 5, these figures are 59% and 33% respectively.

Conclusions

- Pharmacy retail recovery continues, but the situation remains difficult in some regions.

- Market consolidation continues and the largest chains continue to increase the number of pharmacies.

- Pharmacy margins fell to pre-war levels.